HyGOAT insights

The RFNBO Revision Is a Course Correction - But Only for Half the Market

Ekansh Sharma

Founder, HyGOAT | Hydrogen Readiness Research

The EU wants to import 10 million metric tonnes of renewable hydrogen by 2030. It cannot produce that domestically. So why are its rules written as if it can?

This is the central contradiction that emerged from the 1st EU Hydrogen Regulatory Forum in Rotterdam - a gathering I followed closely after parsing all 25 official presentations distributed by DG ENER. The forum confirmed what many in the industry already suspected: the RFNBO Delegated Acts are not working, and a revision is coming faster than the formal July 2028 review deadline.

But the demanded revision overwhelmingly fixes the EU's own bankability problem. And if REPowerEU is to meet its import target, the rulebook also has to work for the producers outside Europe who are supposed to supply the other half.

The Rotterdam Signal: What Eight Member States Demanded

At Rotterdam, Germany, Spain, the Netherlands, Poland, and Austria tabled a formal non-paper calling for swift revision of the RFNBO Delegated Acts - specifically Delegated Acts 2023/1184 and 2023/1185. In the discussion room, Czechia, Hungary, and Italy voiced explicit support, bringing the coalition to eight member states.

Their demands were specific:

- Additionality - extend the transitional period from its current 2028 end-date to 2035, with 10-year grandfathering for early-mover projects already under development

- Temporal Correlation - keep monthly matching in place until at least 2035, and delay the shift to hourly correlation, originally planned for 2030

- Renewable energy share threshold - reduce from 90% to 80%, above which projects don't need to meet sustainability criteria

- Electrolyzer grandfathering - exempt existing electrolysers from retroactive rule changes

Shell asked to extend monthly temporal matching to 2040. RWE flagged that the production-cost-to-willingness-to-pay gap makes RFNBO projects structurally unbankable at current rules. Hydrogen Europe called the DA production rules the single biggest barrier to hydrogen scale-up in Europe.

The EC-commissioned ICF/Fraunhofer ISI study - which interviewed 38 project developers across 19 countries and analysed 73 projects - confirmed the sentiment: "The majority of project developers call for easing requirements." The final results aren't expected until Q4 2026, creating a regulatory vacuum that is already freezing investment decisions.

Why Europe Needs This

I won't argue against the revision. The numbers are alarming.

According to the IEA Global Hydrogen Review 2025, only 4% of announced clean hydrogen projects globally have passed Final Investment Decision. In Europe, the figure is even worse. The chicken-and-egg problem is real: lenders won't finance against a rulebook that might change next year, offtakers won't sign binding long-term agreements without regulatory certainty, and developers can't reach FID without both.

The European Hydrogen Bank's second auction is perhaps the most damning data point. Of the 15 winners, 7 withdrew during grant negotiations - taking with them 1.88 GW of the 2.33 GW allocated (75% of capacity) and EUR 755 million of EUR 993 million in funding. These weren't speculative projects; they were selected winners. The withdrawal rate shows how untenable the current compliance environment is, from selection to execution.

The Oxford Institute for Energy Studies bankability report frames the structural problem well: lenders require investment-grade offtake counterparties, but offtakers won't commit to investment-grade volumes until they have regulatory certainty. You can't break this loop with stricter rules. You break it with clearer, more durable ones.

The relaxation isn't ideology - it's survival. And I mean that literally: European hydrogen developers have spent years and capital designing compliance into projects that may never be viable under the current framework.

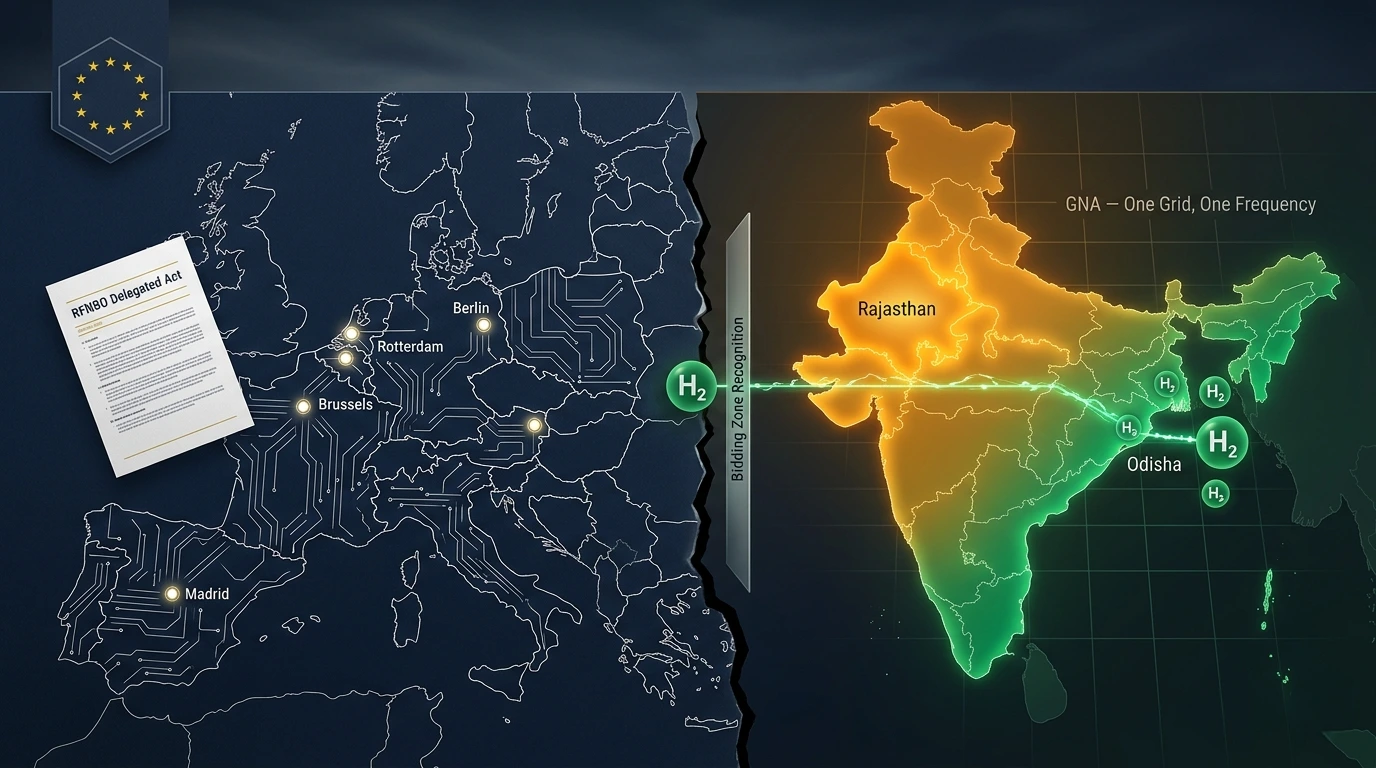

India's Structural Problem: The Geographic Correlation Trap

Now let's talk about what the revision is not addressing.

REPowerEU set a target of 10 MMTPA domestic production and 10 MMTPA of imports of renewable hydrogen by 2030. Half the target depends on supply chains that don't sit within EU borders. And yet the revision focuses almost entirely on the domestic half.

For producers in India - which is positioned as one of the primary export markets for Green Ammonia and green hydrogen into Europe - the most critical problem is geographic correlation, and the current revision demands don't address it.

Here is the technical reality. Article 7.1(a) of Delegated Act 2023/1184 defines geographic correlation by bidding zone: the renewable energy installation and the electrolyzer must sit in the same bidding zone for the renewable electricity to count toward RFNBO compliance.

In theory, this is a reasonable proxy for physical grid connectivity. If the renewable source and the load are in the same price zone, you can reasonably infer that the electrons are flowing through the same system.

In practice, India's grid doesn't map onto this framework.

Data from the Indian Energy Exchange (IEX) shows less than 2% day-ahead price variance across all Indian bid areas for the last three years. This is not a multi-zone market with meaningful price differentiation - it is functionally one grid, operating at near-uniform prices nationwide. India's General Network Access (GNA) mechanism under CERC regulations provides a predetermined power schedule every 15 minutes - legally admissible, granular proof that renewable energy is injected into the grid at a specific time and location.

But the EU does not recognise India as a single bidding zone. Which means a solar farm in Rajasthan powering an electrolyzer at Paradip on the Odisha coast - despite near-zero price variance between them, despite GNA scheduling providing exact 15-minute injection data - does not automatically qualify under RFNBO geographic correlation rules.

The European Commission has hinted that integrated grids without geographically differentiated prices could qualify as a single bidding zone. But "could" is not compliance. You cannot build a $500 million project on regulatory ambiguity.

This is not a technicality. It is a structural disconnect between how India's power market operates and how EU regulators have defined what counts as a "grid."

The Moving Target Problem: Designing Compliance Against a Shifting Rulebook

Let me explain why the revision itself - even if it fixes the EU's bankability problem - creates a parallel problem for non-EU producers.

If you are designing a large-scale Green Ammonia export project in India or the Middle East targeting EU markets, you lock in your project parameters for a decade. The site, the renewable procurement strategy, the electrolyzer specification, the certification pathway under GHCI - these are decisions made years before your first tonne ships.

But regulators are rewriting the rulebook midway. Additionality timelines are shifting. Temporal correlation windows are shifting. Emission intensity thresholds for grid power (Germany has proposed 180 g CO2/kWh in 2028, declining 5 g/year) are entering the rulebook for the first time. The renewable energy share threshold is dropping from 90% to 80%.

Each of these changes solves a problem specific to European producers - operators who have existing electrolyzers that need grandfathering, or PPAs in markets where hourly matching is technically infeasible in the short term. They are legitimate fixes for legitimate European problems.

But for an Indian developer designing compliance into a project that will reach FID in 2027 and begin operations in 2030, every rule change is a parameter that might invalidate a design decision already made. You cannot write a bankable project information memorandum against a rulebook regulators are rewriting to solve someone else's bankability crisis.

The S&P Global analysis of the Hydrogen Bank auction failure frames the issue in capital terms: regulatory uncertainty is not just an inconvenience - it is a risk premium that makes projects non-financeable. That risk premium applies to non-EU producers as much as to European ones. And for exporters, there is an additional layer: not only is the rulebook changing, but the party writing the rulebook has no direct visibility into how the changes interact with the grid and market structures of the exporting countries.

What Good Policymaking Looks Like

I want to be precise here, because I am often misread on this point.

I am not anti-EU. I am not arguing for weaker decarbonisation standards. I am arguing that good policymaking - particularly for a framework as ambitious and globally consequential as RED III - has to balance multiple objectives at once, not just the most politically urgent one.

The four objectives that a revised RFNBO framework should balance:

-

Decarbonisation actually achieved - not just legislated. Rules that no project can comply with don't decarbonise anything. The 4% FID rate is the proof point.

-

Bankability for producers everywhere - not just within EU borders. If the import target is 10 MMTPA and EU domestic production can only realistically deliver a fraction of that by 2030, the rules need to work for the producers who will supply the rest.

-

Global supply chains that can actually deliver - this means recognising that MNRE-regulated green hydrogen certification under GHCI, GNA-based temporal proof, and IEX price data are not second-class forms of compliance evidence. They are what India's grid actually produces. The alternative - requiring Indian projects to comply with a bidding zone framework designed for the EU's internal electricity market - is asking the exporter to conform to the importer's grid architecture.

-

Self-sufficiency as the long-term goal, not protectionism as the short-term default - the revision the 8-state coalition is demanding is the right instinct for the right reasons. But if it primarily protects early EU movers at the expense of import viability, it crosses from pragmatism into protectionism.

The ICF/Fraunhofer study is interviewing developers across 19 countries. When the final results land in Q4 2026, they should reveal whether the revision process incorporates non-EU producers' voices. If it doesn't, the revision will fix half the problem while making the other half harder.

Conclusion: Rules Grounded in Reality, Not Jurisdiction

The hydrogen economy doesn't start with perfect rules. It starts with rules grounded in reality - how grids actually work in India, how projects get financed in the Middle East, how offtake gets committed in a market that doesn't yet have the depth to support investment-grade bilateral contracts.

Rotterdam was a significant moment. Eight member states, unanimous industry demand, and an EC-commissioned study all pointing in the same direction is not a footnote - it's a signal that the political will for revision exists. Based on what I saw in those 25 presentations, my read is that DG ENER will issue a political signal by late 2026, with draft revisions in H1 2027, well ahead of the formal July 2028 deadline.

But "earlier" is not the same as "better." A revision that solves the EU's bankability crisis while leaving the geographic correlation ambiguity for Indian exporters unresolved - while creating new moving-target risks for non-EU project developers - is a half-revision of a half-framework.

REPowerEU's own target is 10 MMTPA of domestic production and 10 MMTPA of imports. If half the target depends on non-EU supply chains, regulators can't write the course correction for one side only.

The question I left Rotterdam asking is the same one I'll be watching through 2026: will the RFNBO revision be written by the producers the EU needs to buy from, or only by the producers it is trying to protect?

Sources

-

European Commission - REPowerEU Strategy (2022) - Target of 10 MMTPA domestic production + 10 MMTPA imported renewable hydrogen by 2030.

-

1st Hydrogen Regulatory Forum, Rotterdam (March 2026) - 8 member states formally demanded RFNBO DA revision via non-paper. Source: Official EC presentations parsed from forum proceedings (25 PDFs).

-

IEA Global Hydrogen Review 2025 - Only 4% of announced clean hydrogen projects globally have reached FID.

-

Argus Media (Sept 2025) - 7 of 15 European Hydrogen Bank auction winners withdrew, representing 75% of allocated capacity and EUR 755M of EUR 993M in funding.

-

Legal500 - "RFNBO Certification: Leveling Dissonances Between EU and Indian Scenarios" - IEX data: less than 2% day-ahead price variance across all Indian bid areas over three years; GNA mechanism provides 15-minute scheduling proof.

-

Norton Rose Fulbright - "Navigating EU RFNBO Regulations: Implications for Green Ammonia Production in India" - Geographic correlation requirement under Art. 7.1(a) of DA 2023/1184; India's bidding zone recognition challenge.

-

AZB & Partners - "General Network Access: One-Nation One-Grid One-Frequency" - GNA regulations under CERC provide non-discriminatory ISTS access with 15-minute block scheduling.

-

S&P Global (Jan 2026) - "European hydrogen industry digests failure of second EU auction."

-

Oxford Institute for Energy Studies (Jan 2026) - "Bankability of Hydrogen Projects: Key Risks, Financing..." - offtake chicken-and-egg problem, lender requirements for investment-grade counterparties.

-

ICF/Fraunhofer ISI - RFNBO Ramp-Up Study (interim, 2026) - EC-commissioned study interviewing 38 developers across 19 countries; majority call for easing requirements. Final results Q4 2026. Source: Presentation 7.2 from Hydrogen Regulatory Forum proceedings.

Frequently Asked Questions

What happened at the 1st EU Hydrogen Regulatory Forum in Rotterdam?

Eight EU member states - Germany, Spain, Netherlands, Poland, Austria, Czechia, Hungary, and Italy - formally demanded a swift revision of the RFNBO Delegated Acts at this forum organised by DG ENER. They called for extended additionality timelines (to 2035), continued monthly temporal correlation (delaying the shift to hourly), and a reduced renewable energy share threshold (from 90% to 80%).

Why are EU hydrogen developers struggling to reach Final Investment Decision?

Only 4% of announced clean hydrogen projects globally have passed FID. The core problem is a chicken-and-egg loop: lenders require binding offtake agreements to finance projects, but offtakers won't commit without regulatory certainty. When the rulebook might change before your project is operational, no lender will underwrite it. The European Hydrogen Bank auction failure - where 7 of 15 winners withdrew, taking 75% of allocated capacity with them - is the clearest evidence of how severe this problem has become.

What is the geographic correlation problem for Indian hydrogen exporters?

RFNBO rules require the renewable energy installation and the electrolyzer to be in the same EU-recognised bidding zone. India's power exchange data shows less than 2% price variance nationwide - it functions as one integrated grid - but the EU does not formally recognise India as a single bidding zone. This means a solar farm in Rajasthan powering an electrolyzer in Odisha may not automatically satisfy geographic correlation requirements, even though India's GNA mechanism provides 15-minute granular proof of renewable injection into the same grid.

How does the RFNBO DA revision affect non-EU hydrogen producers?

The revision creates a moving target. Additionality timelines, temporal correlation windows, and emission intensity thresholds are all shifting to solve problems specific to EU-based producers. For a developer in India or the Middle East designing a $500M project for 2030 delivery, each rule change is a parameter that could invalidate design decisions already made. You cannot bankroll a project against a rulebook regulators are rewriting to solve someone else's problem.

What is India's GNA mechanism and how does it relate to RFNBO compliance?

The General Network Access mechanism, governed by CERC, provides every grid-connected user a predetermined 15-minute power schedule. This schedule is legally admissible proof of renewable energy injection into India's Inter-State Transmission System. In principle, it satisfies the spirit of RFNBO's temporal correlation requirement - granular, time-stamped evidence of renewable use. The unresolved question is geographic correlation: whether the EU will formally recognise India's integrated grid as equivalent to a single bidding zone.